A business credit report provides a comprehensive overview of a company's creditworthiness, helping you make informed decisions when engaging in business transactions. Here's what you need to know about business credit reports:

It typically contains:

A company’s ability to obtain a loan or do business with another business is determined by their business credit score. Businesses’ credit obligations and payback history with lenders and suppliers are used by credit scoring companies to calculate business credit scores, also known as commercial credit scores; any legal filings such as a company’s history, the kind and scale of its business, any liens or judgements it may have, bankruptcies or tax liens, and its repayment record in comparison to other businesses of comparable size.

However, there is a misperception that if a company has good business credit, the owner’s personal credit will never be scrutinized and they will no longer need to put up their own money as collateral for a loan to the company. A personal guarantee may be required for various loans, including bank loans, and many small company creditors assess credit records.

A comprehensive business credit report contains more than just operational information and trade payment history. They are made up of various credit ratings, scores, and statistics, ranging from predictive (for the future) to performance-based (historical), that can be used to demonstrate a business’s dependability and financial stability.

Although the reports from the various credit reporting agencies will differ slightly in appearance, they will all contain similar data. In case you purchase any company credit report, it should contain the following information. In order to successfully navigate the business loan application procedure, it is a good idea to buy a credit report and comprehend it.

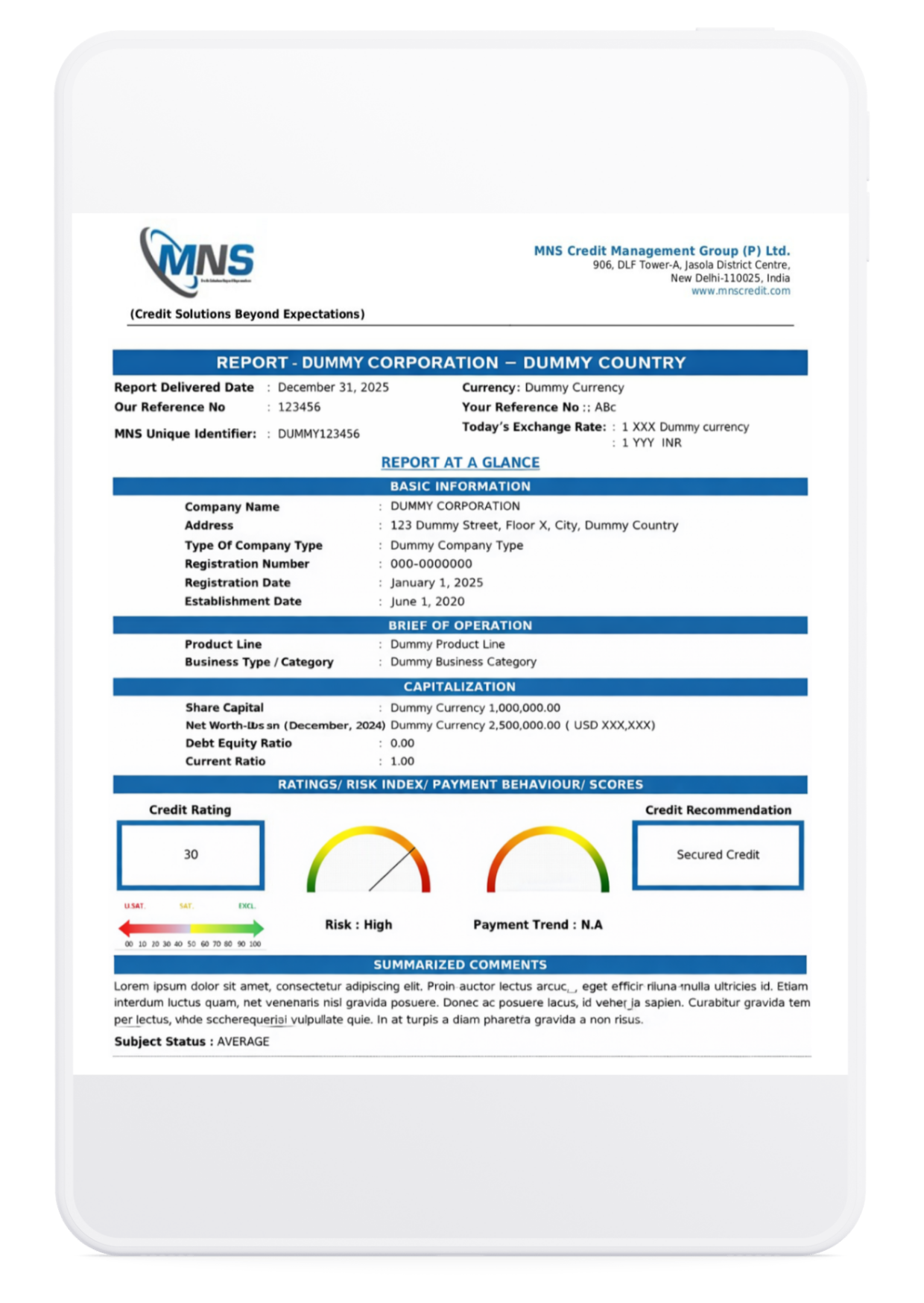

Most likely, the first thing you’ll see on the credit report is your business profile. This section contains the following data:

The section on payment history displays the three-year payment history of your business. Typically, payments made to vendors fall under this category as well. This section also covers payment conditions, the highest credit limit that was recently available, the total credit limit, the monthly payment, and whether it is current or late. Additionally, it will display how frequently you have been 30 days or more late on a tradeline.

The report’s commercial financial history section lists all of the creditors, lenders, and insurers you have made payments to in the past. It displays the terms, the opening date of the tradeline, the original and current balances, and any account delinquencies. Business loans, insurance coverage, credit lines, and related lines will be displayed.

A company credit report will include a credit score, much like a personal credit report. Even while each credit reporting bureau will have its own range of credit scores, they should all produce an easily understandable score. A business credit report should make it obvious what degree of credit risk your firm is at, how that score was calculated, and possibly even a prediction of your company’s future credit risk based on your report.

Your credit capacity, credit history length, and level of delinquency on your report can all have an impact on your company’s credit rating.

MNS Business Information Report gives you comprehensive insights — including MCA company data, credit evaluation, litigation search, global due diligence and screening and more.

Apply Here

The same things that affect your personal credit report also have an impact on your business credit report, but they do so in terms of a business account this time. Let’s look at 3 such important factors that affect your credit report.

Business credit records are maintained by major business credit reporting agencies. Establishing a strong business credit score involves partnering with organizations that report payment histories, making timely payments, and maintaining manageable debt levels. These actions contribute to robust business credit reports, which are crucial for various business operations.

Establishing a business credit score can provide numerous benefits for small firms, including easier access to funding, better business insurance rates, favorable supplier payment terms, and the potential to secure more profitable commercial contracts. Here are some straightforward steps to help your small business establish and enhance its business credit:

A Business Credit Score is a numerical representation of a company's creditworthiness. It evaluates the financial stability and reliability of a business based on factors such as payment history, credit utilization, and financial behavior. The score helps lenders, suppliers, and partners assess the risk of doing business with the company. A higher score indicates lower risk, which can lead to better loan terms and supplier relationships.

There are two metrics to measure creditworthiness – the first is the personal credit score, and the second is the business credit rank.

These metrics are evaluated by lenders before approving a loan. They especially pay close attention to your business credit report and the business’s financial behavior to gauge your creditworthiness. By keeping these healthy, an MSME promoter or owner can get quicker approvals, larger loans, and better interest rates.

Credit report by credit bureaus, such as CIBIL is like a report card that indicates the financial health of a business and helps lending firms decide whether to extend credit to the enterprise or not.

To arrive at a credit score, credit bureaus consider several factors such as the overall amount of loans that the enterprise currently holds, repayment history of loans, and the length of the borrower’s credit history, among other factors.

The rate at which debt is accruing, or the amount and length of recent loans taken out, is another crucial consideration.

Paying your bills on time is one of the best methods to raise your credit score. Your credit score is lowered by defaults, late EMI payments, and rejected checks. Paying the company’s payments on schedule helps you keep excellent ties with creditors and vendors while also raising your credit score.

One of the simple ways to raise your business credit score is to pay off business loans on time, pay your vendors on time, register for a business credit card, keep a close eye on your credit report, etc.

It is true that having good business credit is essential to the success of your company, regardless of the sector you are in. When starting a new business branch or trying to grow an existing one, it is essential to secure financial support. But that will only be the start, it seems. There are some fundamental advantages of having a good business credit score that are undeniable.

Let’s simply be clear about the fact that having good business credit can help you save a lot of money. Creditors will almost always offer you lower interest rates, which are ideal for companies with excellent credit.

Additionally, you have the chance to obtain the best business credit without providing a personal guarantee. The present personal liability is decreased by this part, and the assets you have are protected.

Nothing can compare to the significance of a strong business score if you genuinely want to stay ahead in this fiercely competitive profession. You could always try to retain that higher profit margin that you had intended for yourself, or you could simply pass the interest savings directly on to the clients.

You may always make some selections with the utmost assurance if you have good business credit. The finest thing is that you get all the money you require.

Assess Financial Health: A credit score check gives you a clear picture of your business's financial status, showing how well you manage debt.

Secure Financing: If you plan on applying for loans or lines of credit, lenders will perform a credit score check. Knowing your score ahead of time helps you understand what to expect.

Negotiate Better Terms: Suppliers and vendors may also check your business credit score before offering favorable payment terms. A solid score could lead to better deals.

Monitor for Fraud or Errors: Regular credit score checks allow you to spot discrepancies or fraudulent activities that could hurt your business.

In today’s competitive business environment, having a strong business credit report is crucial. It not only helps you secure loans but also builds trust with customers, partners, and suppliers. A good business credit report can open doors to better financial opportunities, better terms from suppliers, and higher chances of success in your industry.

1. What is a Business Credit Report?

A Business Credit Report (BCR) is a detailed profile of a company’s financial stability, payment history, legal filings, and overall creditworthiness. It helps stakeholders assess the risk of doing business with the company.

2. Why is a Company Credit Report (CCR) important for my business?

A strong Company Credit Report (CCR) facilitates easier access to loans on favorable terms, as it demonstrates financial stability and reliability. Organizations, financial institutions, and business partners review CCRs to identify potential financial or operational risks in business dealings or partnerships.

3. What does a company's credit history represent?

A company's credit history reflects its financial reputation, showcasing how it has managed past debts and loans. This section outlines the business's borrowings, including loans, credit facilities, and any outstanding obligations.

4. What components are included in a CCR?

Key components of a CCR include:

5. What factors negatively impact a CCR?

Several factors can adversely affect a Company Credit Report (CCR) :

Payment History: Late or missed payments can tarnish credit history.

Credit Utilization: High utilization of available credit may indicate financial strain.

Public Records: Involvement in legal issues like bankruptcies can signal financial instability.

6. How can I improve my company's CCR?

Enhancing your CCR involves:

Timely Payments: Consistently pay creditors and suppliers on time.

Monitor Your Report: Regularly review your CCR to identify and rectify errors.

Diversify Credit: Maintain a mix of credit types, such as trade credit and business loans.

7. How Often Should I Check My Business Credit Report?

It’s advisable to check your Business Credit Report at least once a year to ensure its accuracy. Regular checks can help you catch any errors or signs of fraud early and give you a chance to improve your credit score.

8. Can I Improve My Business Credit Score?

Yes, you can improve your Business Credit Score by paying bills on time, reducing credit utilization, maintaining a healthy mix of credit, and correcting any inaccuracies on your credit report. Building a good payment history over time is key to raising your score.

Recommended Read: